Can you negotiate credit card processing fees for your bakery without switching processors or buying new equipment? Yes, and most bakery owners can reduce their effective rate by 0.3% to 0.8% through direct negotiation. That translates to $1,200 to $3,200 in annual savings on $400,000 in card volume. With the Credit Card Competition Act creating unprecedented processor vulnerability in early 2026, bakery owners finally have real leverage at the negotiating table.

You track flour costs down to the gram and labor hours down to the minute. But there's one line item quietly eating 2.5% to 3.5% of your revenue: credit card processing fees. For most bakeries, processing fees rank as the third largest expense after ingredients and payroll. If your bakery processes $40,000 monthly in cards at a 2.8% effective rate, you're handing over $13,440 annually. That's not rent money or an equipment upgrade. It's just gone.

The good news? Right now, in early 2026, you have more negotiating power than you've had in years. New legislation has processors scrambling, and smart bakery owners are using that leverage to claw back thousands. Here's exactly how to do it.

Why Are Credit Card Processing Fees Changing in 2026?

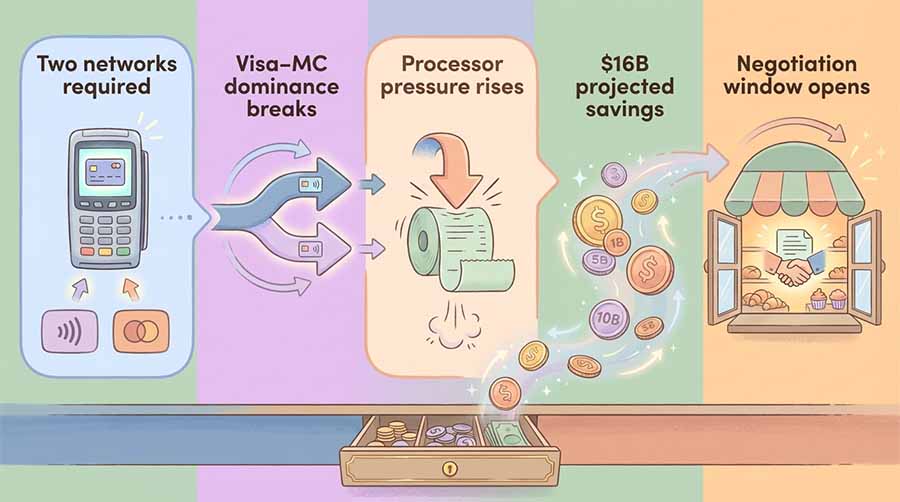

The Credit Card Competition Act was reintroduced in Congress on January 13, 2026. This bill requires banks with over $100 billion in assets to enable at least two unaffiliated payment networks on every credit card, breaking the Visa-Mastercard stranglehold that controls roughly 80% of the US market.

Why processors are suddenly negotiable: They know this legislation could reshape their business model completely. The National Restaurant Association projects this increased competition will save businesses and consumers $16 billion annually. That's real money shifting from card networks back to merchants, and processors want to lock you into contracts before the rules change.

Translation for your bakery: processors who ignored your emails last year are returning calls this year. The next six months represent a narrow but genuine window to negotiate better terms. And with new 2026 tax changes affecting bakery finances, every dollar you save on processing fees matters more than ever.

Which Credit Card Processing Fees Are Negotiable?

Before you negotiate anything, you need to understand what you're actually paying. Your monthly processing statement breaks down into two categories: fees you cannot negotiate and fees you absolutely can.

The Non-Negotiable Fees

Interchange fees go directly to the bank that issued your customer's card. These rates are set by Visa and Mastercard and range from 1.15% to 2.80% depending on card type. A basic Visa credit card costs 1.51% plus $0.10 per transaction. Premium rewards cards cost more.

Assessment fees go to the card networks themselves (Visa, Mastercard, Discover). These typically run 0.13% to 0.15% per transaction. You cannot negotiate these either.

Together, these fixed costs represent roughly 1.3% to 3% of every card transaction. That's your baseline. Everything above that baseline is where negotiation happens.

The Negotiable Markup

Your processor adds their own fees on top of interchange. This is where bakeries get squeezed, and it's 100% negotiable:

| Fee Type | Typical Range | What You Should Pay |

|---|---|---|

| Processing markup | 0.10% to 1.00% | 0.20% to 0.40% |

| Per-transaction fee | $0.05 to $0.30 | $0.10 to $0.15 |

| Monthly account fee | $0 to $25 | $0 to $10 |

| PCI compliance fee | $15 to $30/month | $0 (waived) |

| Statement fee | $10 to $15/month | $0 (waived) |

| Batch fee | $0.10 to $0.25 | $0 |

The hidden fees that add up: Many bakeries pay $15 to $30 monthly for PCI compliance, $10 to $15 for statement fees, and batch fees of $0.10 to $0.25 per day. That's an extra $300 to $600 annually before you process a single card. These fees are almost always waivable if you ask. Controlling processing costs is just one piece of your overall 2026 pricing strategy, but it's one of the easiest to fix.

How to Audit Your Current Processing Costs

Calculate your effective rate by dividing total fees by card volume. Bakeries should target 1.8% to 2.3% for chip transactions.

Pull your last three months of processing statements. You're looking for three numbers:

1. Total card volume: Add up all your Visa, Mastercard, Discover, and Amex sales.

2. Total fees paid: Include everything—transaction fees, monthly fees, PCI fees, all of it.

3. Your effective rate: Divide total fees by total volume. This is your real cost.

Example: $120,000 in card sales, $3,360 in total fees = 2.8% effective rate.

Now compare your effective rate to current bakery benchmarks. Cafes and bakeries with strong chip card usage should target 1.8% to 2.3% effective rates. If you're above 2.5%, you're overpaying.

The Three-Minute Statement Audit

Grab a highlighter and your latest statement. You're looking for hidden charges:

- Circle all monthly fees: PCI compliance, statement fee, account fee, gateway fee

- Highlight your markup rate: Usually labeled "discount rate" or "processing rate" (this is separate from interchange)

- Note your per-transaction fee: Should be $0.10 to $0.15, not $0.25 or higher

- Add up the monthly junk fees: If it exceeds $50, that's your first negotiation target

Pro tip: Take a photo of your marked-up statement. This annotated visual becomes your reference when comparing quotes and makes it easy to spot if processors quietly raise rates later.

Create a simple comparison sheet with three columns: Current Rate, Competitor Quote, Target Rate. When you gather quotes from other processors, this makes it easy to see exactly where you stand and what you're asking for.

How Do Bakeries Negotiate Lower Credit Card Fees?

Step 1: Gather Your Leverage Data

Processors care about two things: your monthly volume and your effective rate. Higher volume gives you more leverage. Prepare a simple one-page summary:

- Average monthly card volume

- Current effective rate

- Length of time with current processor

- Type of transactions (mostly in-person chip vs. keyed-in)

At Plastic Container City, we work with thousands of food professionals across the US, and we consistently see that bakeries with $25,000+ monthly card volume and strong in-person sales get the best terms. If you're processing $40,000 monthly with 95% chip transactions, you're a low-risk, high-value merchant. Remind them of that.

Step 2: Get Competitive Quotes

Contact two to three alternative processors. Tell them exactly what you're paying now and ask for their best rate. Be specific: "I'm currently at 2.6% effective with $40,000 monthly volume. What can you offer?"

Good options: Square Plus, local merchant service providers, and payment-focused fintech companies. Avoid long-term contracts until you've negotiated with your current provider.

Step 3: Calculate Your Switching Cost

Before you threaten to leave, know what leaving actually costs. Check your current contract for early termination fees. Some processors charge $200 to $500 to cancel early. Others have no penalty.

Also factor in hardware costs. If you switch, will you need new card readers? That's $50 to $300 depending on your setup.

When switching makes sense

If your termination fee is under $200 and a competitor offers 0.5% better rates, switching makes financial sense on $30,000+ monthly volume. If your current processor has been responsive and your termination fee is steep, negotiation is smarter.

Step 4: Send the Email Script

Start with email, not a phone call. It creates a paper trail and gives your processor time to check what they can offer.

The email template

Subject: Processing Rate Review – [Your Bakery Name]

Hi [Processor Rep],

I'm reviewing our processing costs and wanted to see if we can improve our current rate. We're processing approximately $[X] monthly at an effective rate of [X]%. I've received quotes from other providers in the 2.1% to 2.4% range with waived monthly fees.

We've been happy with your service, but given our volume and transaction history, I'd like to discuss better terms. Can you review our account and let me know what rates you can offer?

Thanks,

[Your Name]

Keep it short. Don't apologize. Don't over-explain. Just state the facts and ask for better terms.

Step 5: The Phone Follow-Up

If email doesn't get results in 48 hours, call:

"Hi, I sent an email about reviewing our processing rate. I've got quotes from [competitor] at [rate], and I'd prefer to stay with you if we can match or beat that. What can you do?"

What they'll say: "Let me check with my manager." Good. Give them 24 to 48 hours.

What they won't say: "No, we can't budge." If they refuse, switching is your best move.

Most processors will offer something. A typical win: they drop your markup from 0.60% to 0.30% and waive your monthly fees. On $40,000 monthly volume, that's $120 monthly or $1,440 annually.

How Much Can Bakeries Actually Save?

Most bakeries reduce their effective rate by 0.3% to 0.6% via negotiation. This saves $1,500 to $3,000 annually on $40,000 monthly volume.

Let's run the numbers on a typical bakery scenario:

Current state:

- Monthly card volume: $40,000

- Effective rate: 2.8%

- Annual fees: $13,440

After negotiation:

- Monthly card volume: $40,000

- Effective rate: 2.3%

- Annual fees: $11,040

Annual savings: $2,400

That's not life-changing money, but it's real. It's a new deck oven payment. It's a part-time employee for Saturday rushes. It's 10% of your marketing budget. For bakery owners dealing with burnout from 14-hour days, that extra $200 monthly could be the difference between hiring help or running yourself into the ground.

The hidden value: You're also paying fees on tips and sales tax. If your $40,000 monthly includes 20% in tax and tips that aren't actually your revenue, you're paying processing fees on $8,000 of money that never belonged to you. Reducing your rate from 2.8% to 2.3% saves you an extra $40 monthly just on that pass-through money.

When to Switch vs. When to Negotiate

Not every bakery should switch processors. Here's when each strategy makes sense:

Negotiate if:

- Your termination fee exceeds $200

- Your processor has been responsive and helpful

- You're on proprietary hardware that's expensive to replace

- Your effective rate is between 2.2% and 2.6%

Switch if:

- Your effective rate exceeds 2.8%

- You're paying monthly fees above $50

- Your processor is unresponsive or unhelpful

- You're locked into a contract ending within 90 days

The proprietary hardware trap: Processors like Toast and Square offer discounted hardware in exchange for processing exclusivity. That's fine if their rates stay competitive, but if you're stuck with a Toast terminal and want to switch, you'll need to buy new equipment. Factor that into your decision.

What's Your 30-Day Plan to Lower Fees?

Week 1: Audit your last three months of statements. Calculate your effective rate and identify all monthly fees.

Week 2: Request quotes from two alternative processors. Get their offers in writing.

Week 3: Email your current processor with your findings. Reference the Credit Card Competition Act and your competitive quotes.

Week 4: Follow up by phone if needed. Make your decision to stay (with better terms) or switch.

The realistic outcome: Most bakeries that follow this process reduce their effective rate by 0.3% to 0.6%. That's not a miracle, but on $480,000 in annual card volume, it's $1,440 to $2,880 back in your pocket.

Processing fees won't disappear, but you don't have to accept whatever rate your processor assigns you. The 2026 legislative environment has created a genuine opportunity to renegotiate, and bakeries with $25,000+ monthly card volume have real leverage right now.

Pull your statements this week. Run the numbers. Send the email.

Most bakeries that take action reduce their effective rate by 0.3% to 0.6%, saving $1,500 to $3,000 annually without changing how they operate. That money belongs in your business, not in a processor's margin. The processors who have been raising your rates quietly for years? They're finally ready to negotiate. Use it.

A quick note: While these negotiation strategies work for most bakeries, every situation is different. This guide provides general information, not legal or financial advice. Consult with your accountant or financial advisor before making major changes to your payment processing setup.

For more bakery insights, operational tips, and food industry guidance, visit the Plastic Container City blog.

Frequently Asked Questions

Are credit card processing fees negotiable?

Yes. Interchange and assessment fees are set by card networks and non-negotiable, but processor markup, monthly fees, PCI compliance fees, and per-transaction charges are fully negotiable. Bakeries processing $25,000+ monthly typically have the most leverage to reduce their effective rate by 0.3% to 0.8%.

What is a reasonable credit card processing fee for a bakery?

Bakeries should target an effective rate between 1.8% and 2.3% for in-person chip transactions. The average credit card processing fee across all merchants is approximately 2.35%, but bakeries with strong card-present volume and monthly processing above $30,000 can negotiate better terms.

Can you pass credit card processing fees to customers?

Yes, in 48 states. Credit card surcharging is legal everywhere except Connecticut and Massachusetts as of January 2026. Surcharges cannot exceed your actual processing cost, must be clearly disclosed, and can alienate customers. Most bakeries find negotiating lower rates more effective than passing fees to customers.

How to lower card processing fees?

Lower card processing fees by auditing your current statement to identify your effective rate, gathering competitive quotes from at least two alternative processors, and directly negotiating with your current provider using those quotes as leverage. Focus on reducing the processor markup (typically 0.10% to 1.00%) and eliminating monthly fees. The 2026 Credit Card Competition Act gives merchants unprecedented negotiating power right now.

Can I pass credit card fees to customers?

Yes, credit card surcharging is legal in 48 states as of 2026, but prohibited in Connecticut and Massachusetts. New York requires merchants to display the total credit card price upfront. California permits dual pricing but restricts adding fees as separate line items. Most bakeries find that negotiating lower processor rates works better than surcharging, which can alienate regular customers.