Will your bakery overpay taxes in 2026 because you missed a deduction deadline that already passed?

Yes, if you do not fix three things before January 1: how you track staff meals, where you record packaging costs, and when you buy equipment. Section 274(o) eliminates write-offs for most employer-provided meals starting in 2026, but bakeries and restaurants that sell food to customers may qualify for an exception, and most bakery owners have no idea their bookkeeper does not know which rule applies to them

Here are the traps that will cost you money and how to dodge them right now.

Trap 1: You Miss the Equipment Deadline

If you ordered a deck oven in November but it arrives in February, here is what you need to know: you can write off 100% of the cost in 2026 when it gets installed. Not 40%. Not over five years. The full amount.

Why This Matters Today

You have a narrow window right now to decide: buy equipment in December to offset 2025 income, or wait until January when you have a clearer picture of 2026 revenue. The trap is sitting on the fence until March. By then, you have lost the chance to match the deduction to the year that needs it most.

What to do this week: Look at your equipment wish list. If you planned to buy a proofer or display case in Q1 2026, call your CPA today and run the numbers. Figure out which year gets hurt more without the deduction. Then place the order accordingly. Not sure what equipment makes the biggest impact? Check out our guide on must-have baking equipment and supplies for every commercial kitchen.

Bonus Trap: You Don't Track Recipe Development

Testing new recipes in 2025? Those costs are now immediately deductible. The OBBBA restored full expensing for domestic R&D starting in 2025.

What counts: baker wages during testing, trial ingredients, even contractor fees for new product development. A restaurant in Ohio claimed over $50,000 just for test kitchen costs.

What to do now: Pull 2025 invoices labeled "trial batches" or "menu development" and ask your CPA: "Do we qualify for the R&D deduction and credit?"

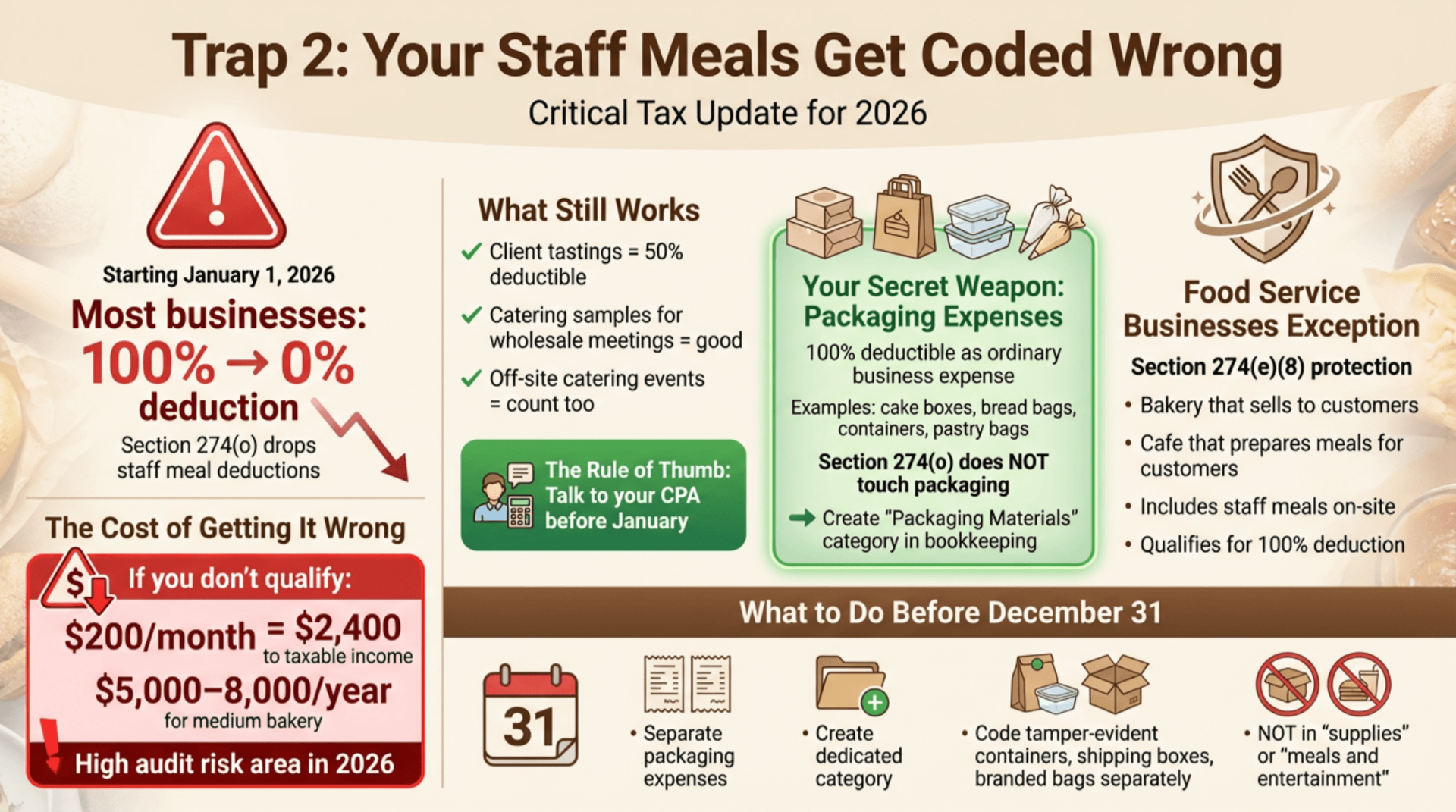

Trap 2: Your Staff Meals Get Coded Wrong

Here is the big one: starting January 1, 2026, most businesses lose deductions for staff meals entirely. Section 274(o) drops them from 100% deductible to zero for most businesses.

But if you run a bakery or cafe that sells food to customers, you likely still qualify for a 100% deduction. Section 274(e)(8) protects food-service businesses that buy ingredients to prepare meals for customers—including meals your team eats on-site.

The trap: your bookkeeper will code these wrong in 2026, either marking everything non-deductible (costing you money) or marking everything deductible without checking if you qualify (triggering an audit).

What Still Works

Client tastings? Still 50% deductible. Catering samples you bring to a wholesale meeting? Still good. Meals at an off-site catering event? Those count too.

The Rule of Thumb: Talk to your CPA before January. If you qualify for the Section 274(e)(8) exception, your staff meals stay deductible. If you do not, they go to zero. Do not guess, this is a high-audit-risk area in 2026.

The key difference: meals for YOUR benefit versus meals for THEIR convenience. If you feed your staff so they can work through lunch, that is now non-deductible. If you feed a potential client to close a deal, you are fine.

The math is simple: if you spend $200/month on staff meals and don't qualify for the bakery exception, you just added $2,400 to your taxable income. A cafe with a dozen employees eating regularly can easily hit $5,000–$8,000.

Your Secret Weapon: Packaging Expenses

Here is your break. Every cake box, bread bag, clamshell container, and pastry bag you buy remains 100% deductible as an ordinary business expense. Packaging is not a meal. It is not entertainment. Section 274(o) does not touch it.

Most bakery owners lump packaging into "supplies" and move on. Big mistake. Starting in 2026, when employer-provided meal deductions shrink or disappear, packaging remains one of the few food-related expenses you can always write off at 100% without any Section 274 limitations. Poor packaging tracking can quietly cost your bakery thousands in lost deductions every year.

What to do before December 31: Separate every packaging expense into its own category. Create a line called "Packaging Materials" in your bookkeeping software. When you buy tamper-evident containers, insulated shipping boxes, or branded pastry bags, code them there. Not in "supplies." Not in "meals and entertainment." Keep them clean.

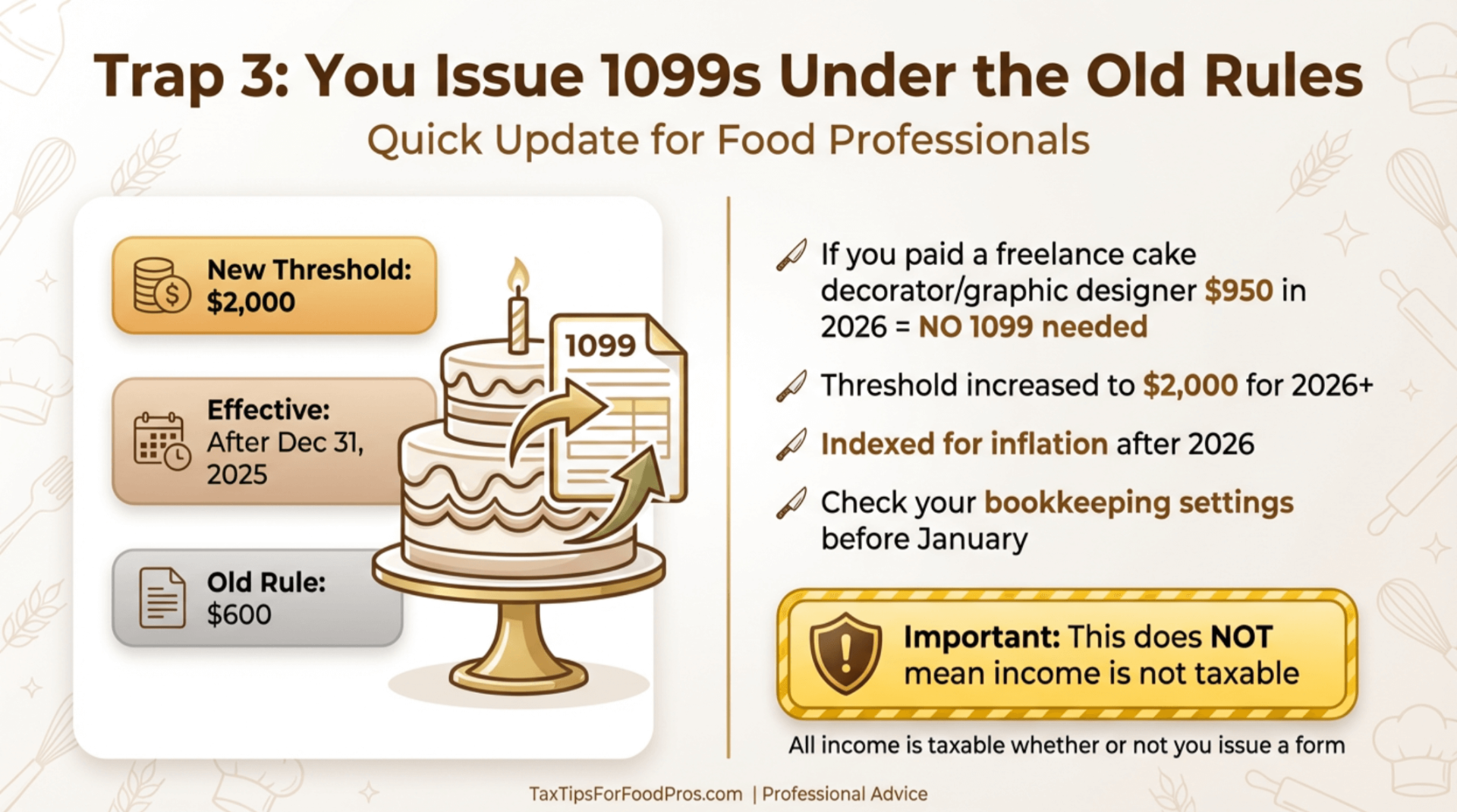

Trap 3: You Issue 1099s Under the Old Rules

Quick one: if you paid a freelance cake decorator or graphic designer $950 in 2026, you do not owe them a 1099. The threshold just jumped to $2,000 for payments made after December 31, 2025 and will be indexed for inflation after 2026.

The trap is your bookkeeping software might not update automatically. If it still flags everyone over $600, you will waste time generating unnecessary forms. Check your settings before January.

One important note: This does not mean your decorator skips reporting that $950. All income is taxable whether or not you issue a form. It just means less paperwork for you.

Trap 4: Your Tip Credit Gets Missed

If you run a bakery cafe where customers tip at the counter and your team pools those tips, you might qualify for a credit against your FICA taxes. The FICA tip credit just expanded to cover more types of tipped services.

The trap: most small bakeries never claim this because they assume it only applies to full-service restaurants. Wrong. If your staff gets tips and you pay the employer share of FICA on those tips, you can get money back.

What to do now: Call your payroll provider before you file and ask if you qualify. Many bakery owners leave hundreds or thousands on the table every year simply because they do not know this credit exists.

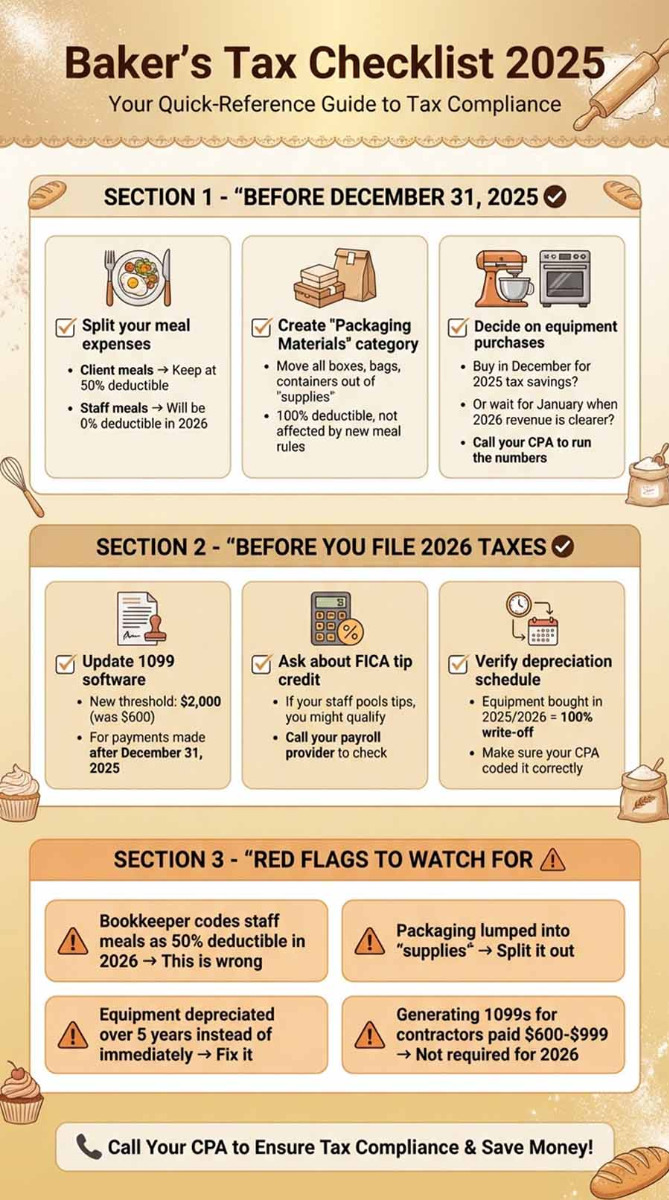

Your Quick-Reference Checklist

Here is exactly what to do this week to dodge these traps

The Bottom Line

The biggest trap is assuming your CPA will catch these changes automatically. Many bakery owners find that generalist accountants miss hospitality-specific rules like the meal deduction changes or fail to separate packaging from supplies, simply because they handle dozens of industries and cannot track every sector's nuances.

If you hand them a shoebox of receipts in March, they will code meals as 50% deductible because that is what they did last year. You will overpay, and you will never know it happened.

Bakery owners who fix their bookkeeping in December will save money. Bakery owners who wait until April will just pay more taxes. It is that simple.

For more bakery insights, business strategy tips, and food-industry updates, visit the Plastic Container City blog.

Frequently Asked Questions

Does the 21% corporate tax rate expire?

No. The 21% corporate rate remains in effect under current law and does not have a scheduled expiration date. However, Congress can always change tax rates through future legislation.

What is the tax cut for July 1 2025?

No federal tax cut took effect specifically on July 1, 2025. The One Big Beautiful Bill Act (OBBBA) was signed into law in July 2025, but most provisions apply to tax years 2025 or 2026, not as a mid-year rate change.

Can I deduct the cost of testing new recipes?

Yes. Starting in 2025, domestic R&D costs, including wages for developing new recipes and ingredients used in testing, are immediately deductible under Section 174A. You may also qualify for the R&D tax credit, which can offset your tax liability dollar-for-dollar. Ask your CPA if your recipe development qualifies.

Do I need to issue a 1099 to a contractor I paid $1,500 in 2026?

No. The threshold for 1099-MISC/NEC increased to $2,000 for payments made after December 31, 2025. However, the contractor must still report all income regardless of whether you issue a form.

What happens when I hit the next tax bracket?

Only the dollars above the threshold get taxed at the higher rate. If you're single and earn $100,000, your first chunk gets taxed at 10%, the next at 12%, then 22%, and so on. Crossing into the 24% bracket does not mean your entire income is taxed at 24%—only the amount over the threshold.